5 May 2026

5 May 2026 Urban Fiscal Dynamics: Tracking Pune’s Financial Evolution

The fiscal architecture of the Pune Municipal Corporation (PMC) is currently undergoing a structural transition that serves as a profound case study in urban public policy and municipal finance. Historically recognized as the cultural and educational capital of Maharashtra, Pune has transformed into a major global hub for information technology and automotive manufacturing, driving a consistent need for sophisticated urban governance. In the past, the city’s budgetary scenario was characterized by a relatively compact geographic focus, with revenue streams anchored primarily by Octroi and subsequently Local Body Tax (LBT). These streams provided a steady, albeit traditional, financial base that supported a steady pace of internal development. However, in recent years, the corporation has expanded its jurisdiction to 516 square kilometres, becoming the largest municipal body in Maharashtra by area. This expansion represented a significant institutional milestone that required a strategic realignment of the city’s revenue and expenditure frameworks. By merging 34 peripheral villages into its limits (11 in 2017 and 23 in 2021), the PMC effectively invited a capital intensive model. This shifted the political economy of the city from maintaining infrastructure in established wards to the massive task of providing urban grade services to formerly semi-rural peripheries. This analysis explores the trajectory of this metamorphosis from 2022-23 to 2026-27, examining how the city has balanced its expanding ambitions against the hard realities of revenue realization.

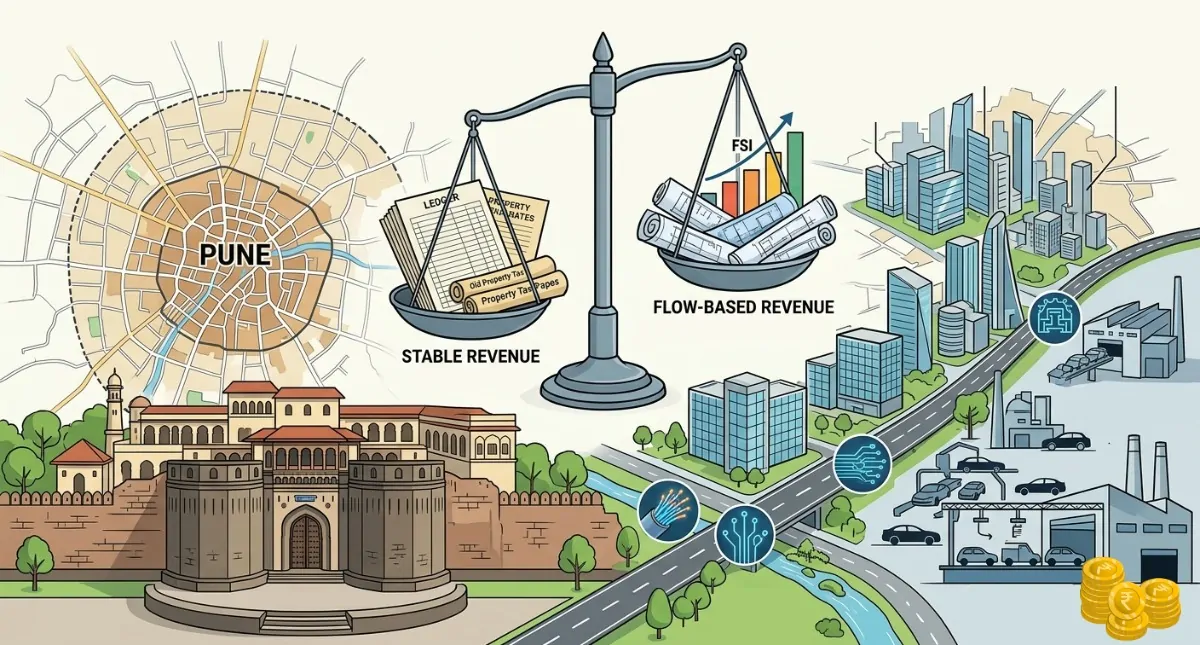

Central to the financial health of any urban local body is the concept of fiscal autonomy, often measured by the Self Reliance Ratio. In public finance, this ratio indicates a municipality’s ability to fund its activities through own source revenue rather than state or central government grants. In the decade preceding 2020, the PMC raised around 43% of its total revenue (actuals) from own-sources of revenue, of which approximately 50 per cent came from the property tax collections. However, between 2022 and 2027, the PMC seems to have maintained a high-level degree of self-sufficiency, with own source revenue frequently exceeding 75% to 80% of total income (budgeted). But, a deeper dive into the data reveals that the qualitative nature of this revenue has undergone a risky shift. Historically, the bedrock of Pune’s finance was stock based taxes, primarily Property Tax, which provides a stable and predictable cash flow. However, over the past 3-4 years the balance has tipped toward flow based streams, specifically building development premiums and FSI charges. According to the 2026-27 budget, nearly 30% of the city’s income is tethered to construction activity. While this construction led financing model allows the city to front load massive infrastructure projects without incurring heavy external debt, it introduces a pro cyclical risk. In public policy terms, this means that during a real estate downturn, the very funds required to maintain the newly built suburban infrastructure could evaporate, potentially leading to a maintenance deficit that could plague the city’s balance sheet for decades.

This shift in revenue composition is mirrored by a widening gap in the city’s budgetary forecasting. A longitudinal look at the data from 2010-11 to 2026 reveals a concerning trend where budgetary estimates have become increasingly decoupled from administrative collection capacity. The actual budget realisation is on an average around 77%, with the highest being 90% in 2015-16 and the lowest being 64.8 percent in 2016-17. This 20% gap is a classic symptom of optimism bias in municipal budgeting. When targets are set aggressively to accommodate high profile political promises, such as flyovers and riverfront development, it creates a false sense of fiscal space. In reality, when the actual revenue falls short, the administration is forced into emergency expenditure rationalization. This usually results in the crowding out of essential but less visible projects, such as sewage treatment maintenance, digital governance upgrades, and environmental conservation efforts, which often see their funding diverted to cover the shortfall of massive asphalt heavy projects.

The expenditure side of the PMC’s ledger reveals a similarly complex struggle between recurring obligations and growth oriented investments, often described in public policy as the dilemma between people and asphalt. As of the 2026-27 budget, the corporation’s establishment costs, which include salaries, pensions, and contractual wages, have scaled significantly. This is largely due to the absorption of administrative staff and service requirements from the 34 merged villages. With a core salary outlay now pegged at approximately 3,881 crore rupees annually. This fixed cost is inflexible. Unlike capital projects, salaries cannot be deferred. When establishment costs consume a growing portion of the revenue surplus, it creates a fiscal lock in. Currently, these ‘people related’ costs account for nearly 22% to 25% of total expenditure. While this is lean compared to many global cities, the rapid growth in this segment requires a corresponding, permanent increase in recurring revenue to ensure the city does not face a liquidity crisis in the next decade.

Simultaneously, the city has maintained an aggressive Capital Expenditure intensity, targeted at over 40% for the 2026-27 fiscal year. This is a vital metric for a growing city, as it measures the portion of the budget dedicated to creating long term assets rather than just keeping the lights on. However, the distribution of this spending is heavily skewed toward Urban Mobility. With 1,800 crore rupees allocated to roads and flyovers, the PMC is pursuing a connectivity first policy. The underlying logic is that improved throughput will spur economic activity and, by extension, real estate premiums. Yet, this focus comes at a strategic cost to soft infrastructure. For instance, the combined budget for Information Technology and the Environment department remains less than 1% of the total outlay. From a public policy standpoint, this suggests a city that is expanding its physical skeleton at the expense of its digital and ecological nervous systems. Without investing in flood management, urban heat island mitigation, and smart governance, the high speed roads being built today may lead to a city that is physically connected but environmentally and administratively fragile.

Another critical dimension of the PMC’s current trajectory is the strategic use of market linked financing. The Pune Municipal Corporation is increasingly exploring market-based financing, with plans in the 2026–27 budget to raise around ₹500 crore through municipal bonds. This reflects a shift toward project-based funding, where infrastructure projects are expected to generate their own revenue. However, raising funds is only one part of the challenge. The real concern lies in whether the PMC has the administrative capacity to use these funds effectively and on time.

In the past, the corporation has struggled to fully utilise bond proceeds, which risks increasing interest costs without creating corresponding assets. Unless the PMC strengthens its project management systems and ensures stable user charges, the burden of repaying this debt may ultimately fall on its general revenues, putting additional pressure on already unstable income sources like construction-related revenues

The inclusion of the 34 merged villages also introduces a unique challenge of horizontal equity in public spending. Older city wards, which contribute the lion’s share of property tax, often demand a commensurate level of service and beautification. Meanwhile, the newly merged peripheries require basic survival infrastructure including drainage, street lighting, and primary health centers. The 2026-27 budget attempts to bridge this by allocating nearly 954 crore rupees specifically to these new zones. However, this creates a political economic friction within the Standing Committee. Balancing the luxury needs of the core city with the basic needs of the periphery is the defining public policy tightrope of this decade. If the PMC fails to deliver visible improvements in the merged villages, it risks an urban decay at the edges that will eventually drag down the economic productivity of the entire metropolitan area.

In conclusion, the fiscal state of Pune from 2022 to 2027 characterizes a city in a high growth, high risk phase. The PMC has shown incredible resilience by maintaining a high self-reliance ratio during a period of massive geographic scaling. By monetizing its role as a planning authority, it has successfully funded the initial waves of suburban expansion. However, the data warns that this model is approaching its limits. The widening realization gap, the volatility of real estate premiums, and the rising burden of fixed establishment costs suggest that the phase of easy growth is over.

For Pune to avoid a fiscal plateau, the next five years of public policy must focus on revenue consolidation and diversification. This means moving away from the transaction based model of development premiums and toward a service based model of optimized property taxes and equitable user fees. Furthermore, the city must rebalance its capital spending away from just asphalt and toward digital and environmental resilience. Only by maturing its financial architecture to match its new geographic scale can the Pune Municipal Corporation ensure its position as a growing economic hub in western India. The transition from a city of roads to a city of services will be the ultimate test of its fiscal and administrative legacy.

-Dr. Saylee Jog

Assistant Professor.

Gokhale Institute of Politics and Economics